Forecast OSEM model

forecast_model.RdForecast OSEM model

Usage

forecast_model(

model,

exog_predictions = NULL,

n.ahead = 10,

ci.levels = c(0.5, 0.66, 0.95),

exog_fill_method = "AR",

ar.fill.max = 4,

plot = TRUE,

uncertainty_sample = 100,

quiet = FALSE

)Arguments

- model

A model object of class 'osem'.

- exog_predictions

A data.frame or tibble with values for the exogenous values. The number of rows of this data must be equal to n.ahead.

- n.ahead

Periods to forecast ahead

- ci.levels

Numeric vector. Vector with confidence intervals to be calculated. Default: c(0.5,0.66,0.95)

- exog_fill_method

Character, either 'AR', 'auto', or 'last'. When no exogenous values have been provided, these must be inferred. When option 'exog_fill_method = "AR"' then an autoregressive model is used to further forecast the exogenous values. With 'last', simply the last available value is used. 'auto' is an

auto.arimamodel.- ar.fill.max

Integer. When no exogenous values have been provided, these must be inferred. If option 'exog_fill_method = "AR"' then an autoregressive model is used to further forecast the exogenous values. This options determines the number of AR terms that should be used. Default is 4.

- plot

Logical. Should the result be plotted? Default is TRUE.

- uncertainty_sample

Integer. Number of draws to be made for the error bars. Default is 100.

- quiet

Logical. Should messages about the forecast procedure be suppressed?

Value

A list of class 'osem.forecast' with the following elements:

- forecast

A tibble with the forecasted values for each module.

- orig_model

The original model object of class 'osem'.

- dictionary

The dictionary used for the model.

- exog_data

A tibble with the exogenous data used for the forecast.

- exog_data_nowcast

A tibble with the exogenous data used for the nowcasting.

- nowcast_data

A tibble with the nowcasted data.

- args

A list with the arguments used for the forecast.

- full_forecast_data

A tibble with the full forecast data, if available.

Examples

spec <- dplyr::tibble(

type = c(

"d",

"d",

"n"

),

dependent = c(

"StatDiscrep",

"TOTS",

"Import"

),

independent = c(

"TOTS - FinConsExpHH - FinConsExpGov - GCapitalForm - Export",

"GValueAdd + Import",

"FinConsExpHH + GCapitalForm"

)

)

# \donttest{

spec <- dplyr::tibble(

type = c(

"d",

"d",

"n"

),

dependent = c(

"StatDiscrep",

"TOTS",

"Import"

),

independent = c(

"TOTS - FinConsExpHH - FinConsExpGov - GCapitalForm - Export",

"GValueAdd + Import",

"FinConsExpHH + GCapitalForm"

)

)

a <- run_model(specification = spec,

input = sample_input,

primary_source = "local",

constrain.to.minimum.sample = FALSE)

#>

#> --- Estimation begins ---

#> Estimating Import = FinConsExpHH + GCapitalForm

#> Constructing TOTS = GValueAdd + Import

#> Constructing StatDiscrep = TOTS - FinConsExpHH - FinConsExpGov - GCapitalForm - Export

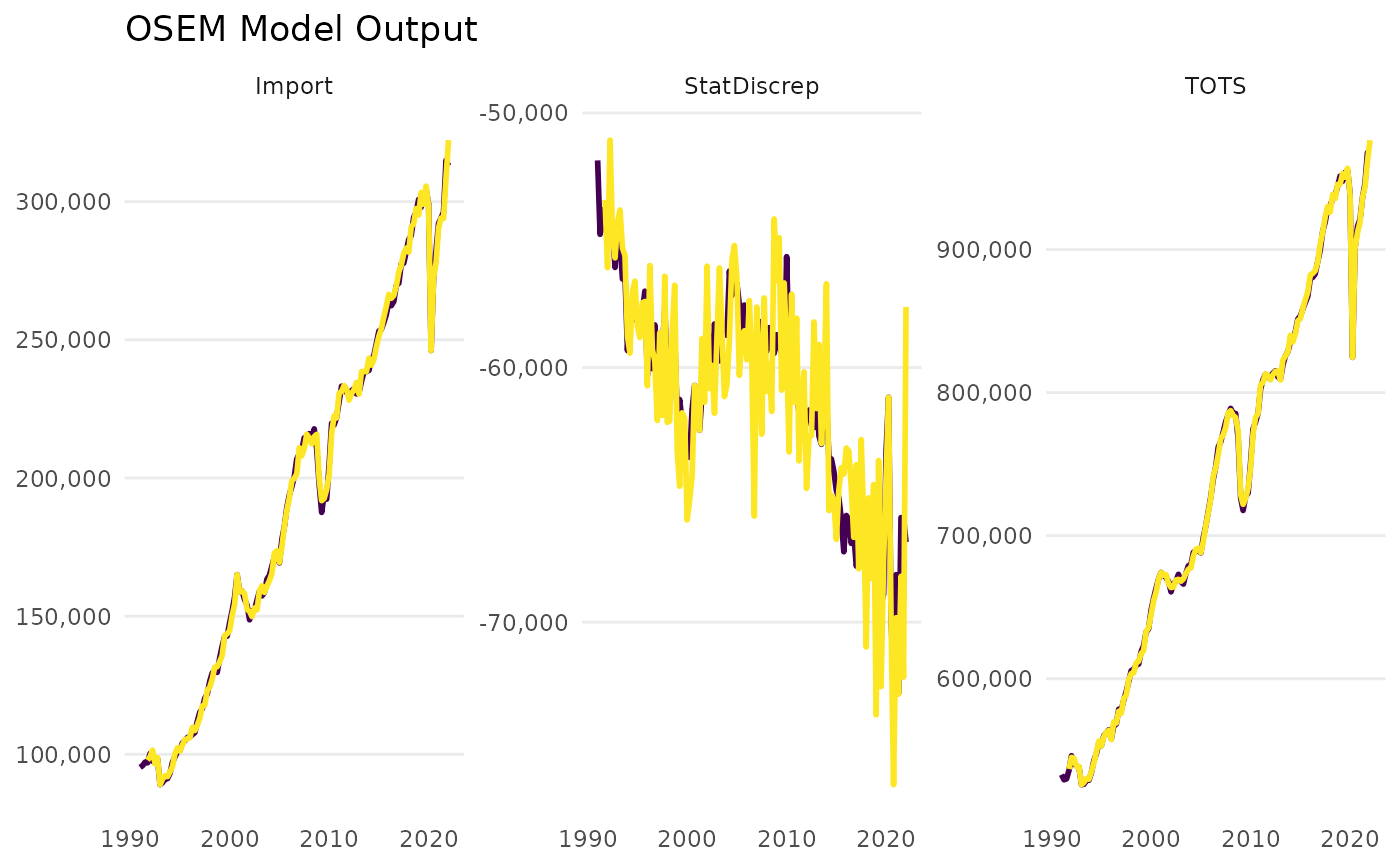

forecast_model(a)

#> No exogenous values provided. Model will forecast the exogenous values with an AR4 process (incl. Q dummies, IIS and SIS w 't.pval = 0.001').

#> Alternative is exog_fill_method = 'last'.

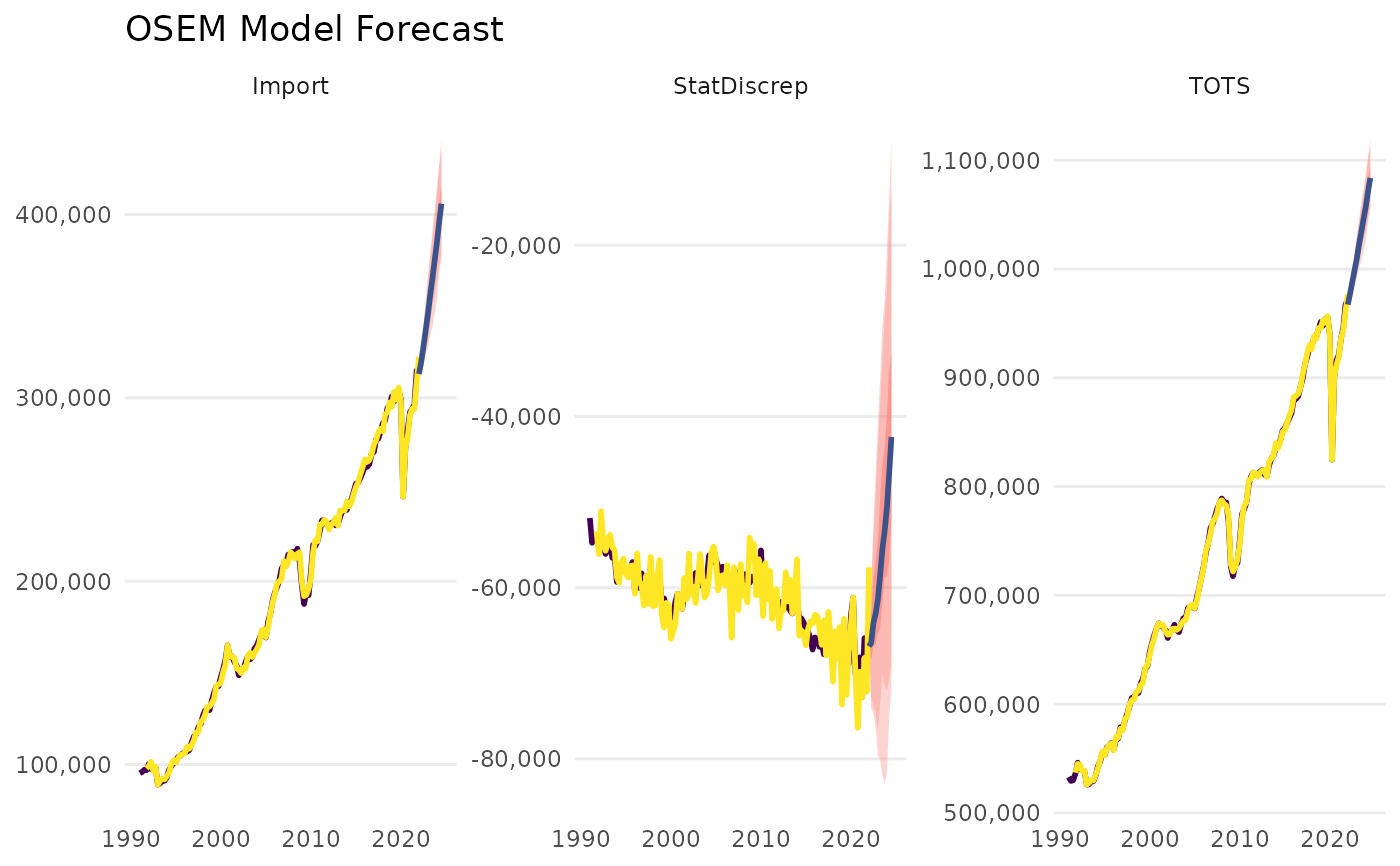

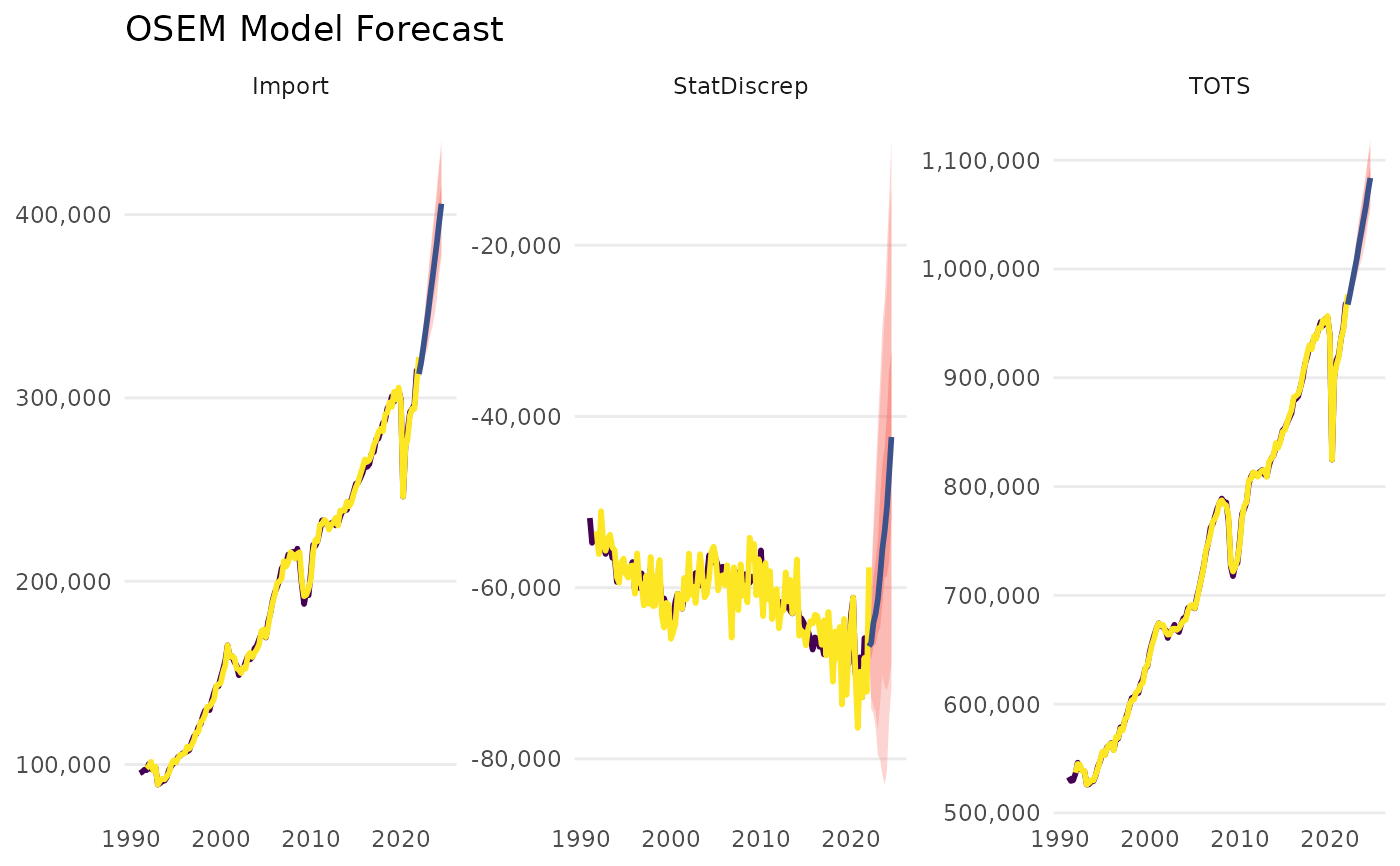

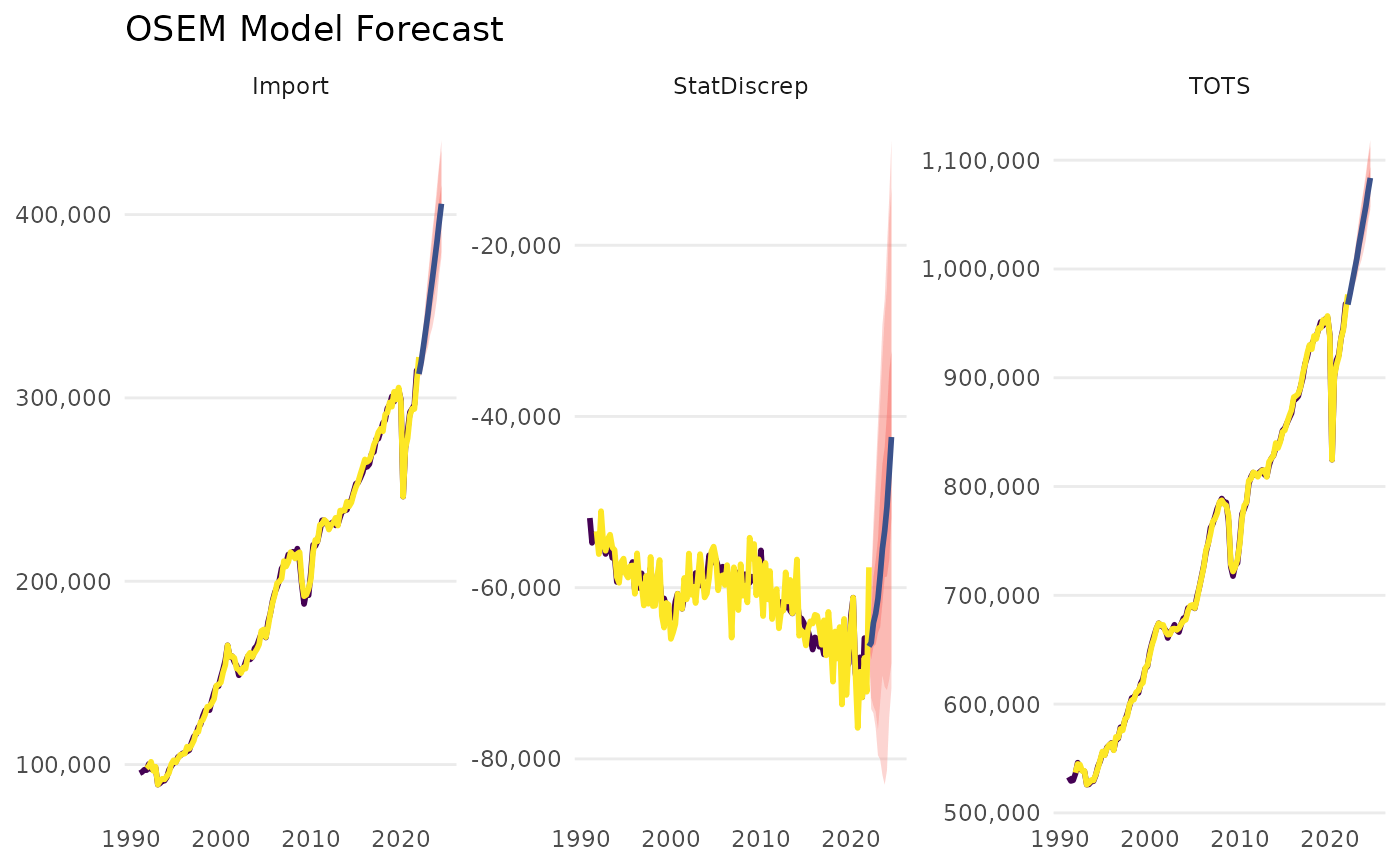

forecast_model(a)

#> No exogenous values provided. Model will forecast the exogenous values with an AR4 process (incl. Q dummies, IIS and SIS w 't.pval = 0.001').

#> Alternative is exog_fill_method = 'last'.

#> OSEM Model Forecast Output

#> -----------------------

#>

#> Forecast Overview:

#> Forecast Horizon: 2022-07-01 to 2024-10-01

#> Forecast Method: AR Model (Outlier and Step Shift Corrected)

#> Max AR Length: 4

#>

#> Central Forecast Estimates:

#> # A tibble: 10 × 4

#> Date Import TOTS StatDiscrep

#> 1 2022-07-01 46750. 118296. -8925.

#> 2 2022-10-01 47461. 120244. -8117.

#> 3 2023-01-01 47439. 121404. -7812.

#> 4 2023-04-01 47386. 122288. -7748.

#> 5 2023-07-01 47720. 124005. -7287.

#> 6 2023-10-01 47817. 125479. -6636.

#> 7 2024-01-01 48119. 127175. -6181.

#> 8 2024-04-01 48028. 128609. -5880.

#> 9 2024-07-01 48208. 130441. -5455.

#> 10 2024-10-01 48509. 132521. -4652.

#> OSEM Model Forecast Output

#> -----------------------

#>

#> Forecast Overview:

#> Forecast Horizon: 2022-07-01 to 2024-10-01

#> Forecast Method: AR Model (Outlier and Step Shift Corrected)

#> Max AR Length: 4

#>

#> Central Forecast Estimates:

#> # A tibble: 10 × 4

#> Date Import TOTS StatDiscrep

#> 1 2022-07-01 46750. 118296. -8925.

#> 2 2022-10-01 47461. 120244. -8117.

#> 3 2023-01-01 47439. 121404. -7812.

#> 4 2023-04-01 47386. 122288. -7748.

#> 5 2023-07-01 47720. 124005. -7287.

#> 6 2023-10-01 47817. 125479. -6636.

#> 7 2024-01-01 48119. 127175. -6181.

#> 8 2024-04-01 48028. 128609. -5880.

#> 9 2024-07-01 48208. 130441. -5455.

#> 10 2024-10-01 48509. 132521. -4652.

# }

# }