Runs the OSEM model

run_model.RdRuns the OSEM model according to the given specification of modules.

Usage

run_model(

specification,

dictionary = NULL,

input = NULL,

primary_source = c("download", "local"),

save_to_disk = NULL,

use_logs = "both",

trend = TRUE,

ardl_or_ecm = "ardl",

max.ar = 4,

max.dl = 4,

saturation = c("IIS", "SIS"),

saturation.tpval = 0.01,

max.block.size = 20,

gets_selection = TRUE,

selection.tpval = 0.01,

constrain.to.minimum.sample = TRUE,

keep = NULL,

pretest_steps = FALSE,

present = FALSE,

quiet = FALSE,

plot = TRUE,

inputdata_directory = NULL,

cvar.ar = 2,

coint_seasonal = FALSE,

coint_deterministic = "const",

coint_significance = "5pct"

)Arguments

- specification

A tibble or data.frame with three columns. Column names must be: 'type', 'dependent', and 'independent'. The column 'type' must contain for each row a character of either 'd' (Identity) or 'n' (Definition - i.e. will be estimated). The column 'dependent' must contain the LHS (Y variables) and the column named 'independent' containing the RHS (x variables separated by + and -).

- dictionary

A tibble or data.frame storing the Eurostat variable code in column 'eurostat_code' and the model variable name in 'model_varname'. If

download == TRUEthen the dictionary also requires a column named 'dataset_id' that stores the Eurostat dataset id. WhenNULL, the default dictionary is used.- input

Character vector or list. An argument to directly pass input files for the OSEM model to be run. Can include a character path to .xlsx, .csv or .rds input files in which the data is stored. Cannot be

NULLifdownload == FALSE.- primary_source

A string. Determines whether

"download"or"local"data loading takes precedence.- save_to_disk

A path to a directory where the final dataset will be saved, including the file name and ending. Not saved when

NULL.- use_logs

To decide whether to log any variables. Must be one of 'both', 'y', 'x', or 'none'. Default is 'both'.

- trend

Logical. Should a trend be added? Default is TRUE.

- ardl_or_ecm

Either 'ardl' or 'ecm' to determine whether to estimate the model as an Autoregressive Distributed Lag Function (ardl) or as an Equilibrium Correction Model (ecm).

- max.ar

Integer. The maximum number of lags to use for the AR terms. as well as for the independent variables.

- max.dl

Integer. The maximum number of lags to use for the independent variables (the distributed lags).

- saturation

Carry out Indicator Saturation using the 'isat' function in the 'gets' package. Needs a character vector or string. Default is 'c("IIS","SIS")' to carry out Impulse Indicator Saturation and Step Indicator Saturation. Other possible values are 'NULL' to disable or 'TIS' or Trend Indicator Saturation. When disabled, estimation will be carried out using the 'arx' function from the 'gets' package.

- saturation.tpval

The target p-value of the saturation methods (e.g. SIS and IIS, see the 'isat' function in the 'gets' package). Default is 0.01.

- max.block.size

Integer. Maximum size of block of variables to be selected over, default = 20.

- gets_selection

Logical. Whether general-to-specific selection using the 'getsm' function from the 'gets' package should be done on the final saturation model. Default is TRUE.

- selection.tpval

Numeric. The target p-value of the model selection methods (i.e. general-to-specific modelling, see the 'getsm' function in the 'gets' package). Default is 0.01.

- constrain.to.minimum.sample

Logical. Should all data series be constrained to the minimum data series? Default is

TRUE.- keep

Character. A string that will be used as regex (in

grepl()) when selection is carried out. This argument therefore requiresgets_selection = TRUE. Variables that match this character will not be selected over (seegetsmfor details).- pretest_steps

Logical. Default is

FALSE. This argument controls whether isat should first be run for SIS in isolation before other saturation methods are added (IIS, TIS). This can lead to better results if there are many IIS identified at the end of the estimation sample/forecast origin. IfTRUEthenisatis first carried out just for SIS (if activated using 'sis = TRUE'), then the SIS breaks are pre-entered to anotherisatestimation but not selected over. After both isat runs, a union model selection is done usinggets.- present

A logical value whether the final OSEM model output should be presented or not.

- quiet

Logical with default = FALSE. Should messages be displayed? These messages are intended to give more information about the estimation and data retrieval process.

- plot

Logical with default = TRUE. Should plots be displayed?

- inputdata_directory

Deprecated. Use 'input' instead. Functionality of specifying a directory is retained for now but this argument will be removed in the future.

- cvar.ar

Number of lags of the VAR system in levels. Must be > 2.

- coint_seasonal

Logical value whether cointegration analysis should include seasonal dummies.

- coint_deterministic

Character specifying whether and if yes which deterministic component to include in the cointegrating relationship.

- coint_significance

Significance level for the rank test for cointegration. Can only be one of '1pct', '5pct', '10pct'.

Value

An object of class osem.

Examples

spec <- dplyr::tibble(

type = c(

"d",

"d",

"n"

),

dependent = c(

"StatDiscrep",

"TOTS",

"Import"

),

independent = c(

"TOTS - FinConsExpHH - FinConsExpGov - GCapitalForm - Export",

"GValueAdd + Import",

"FinConsExpHH + GCapitalForm"

)

)

# \donttest{

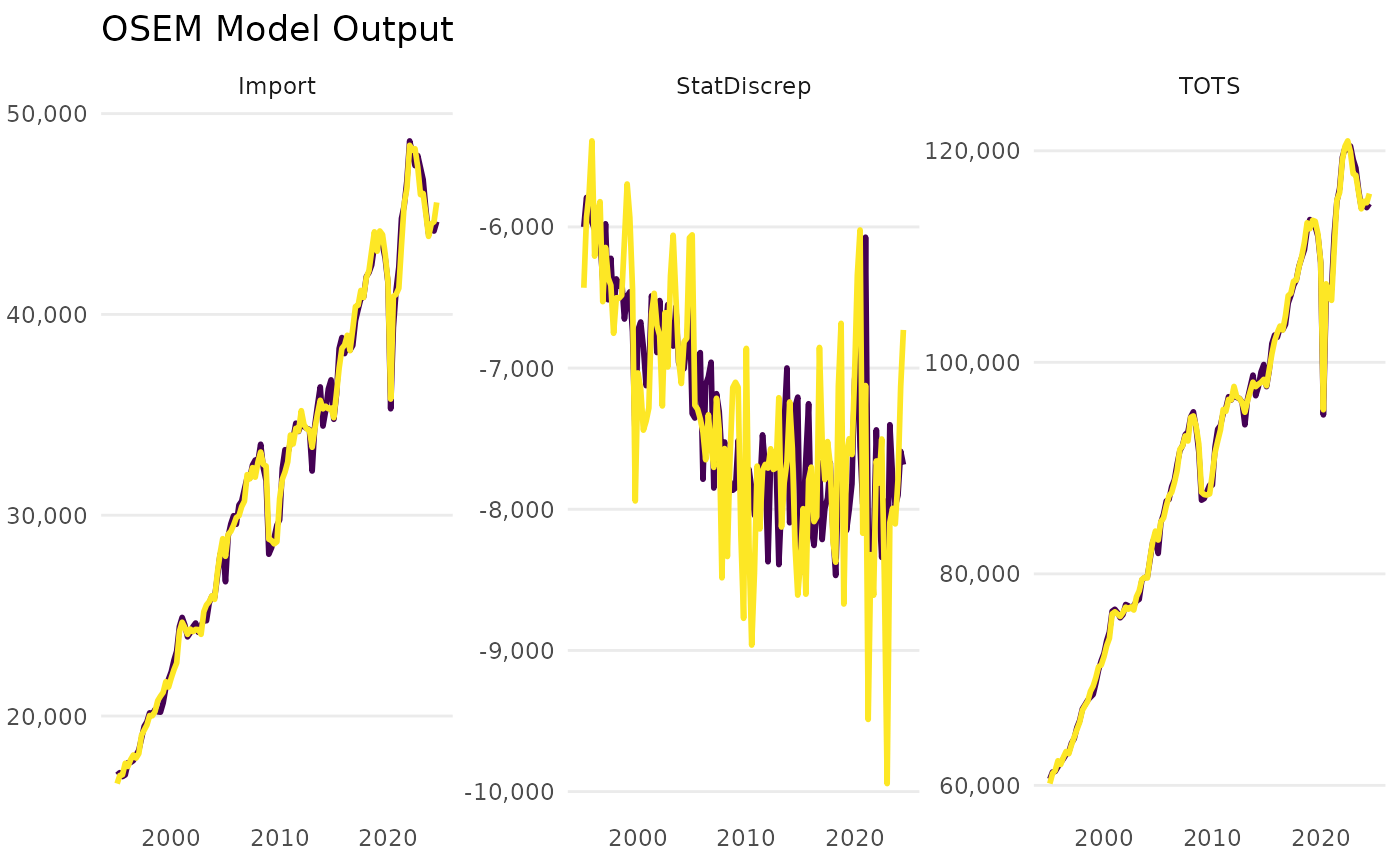

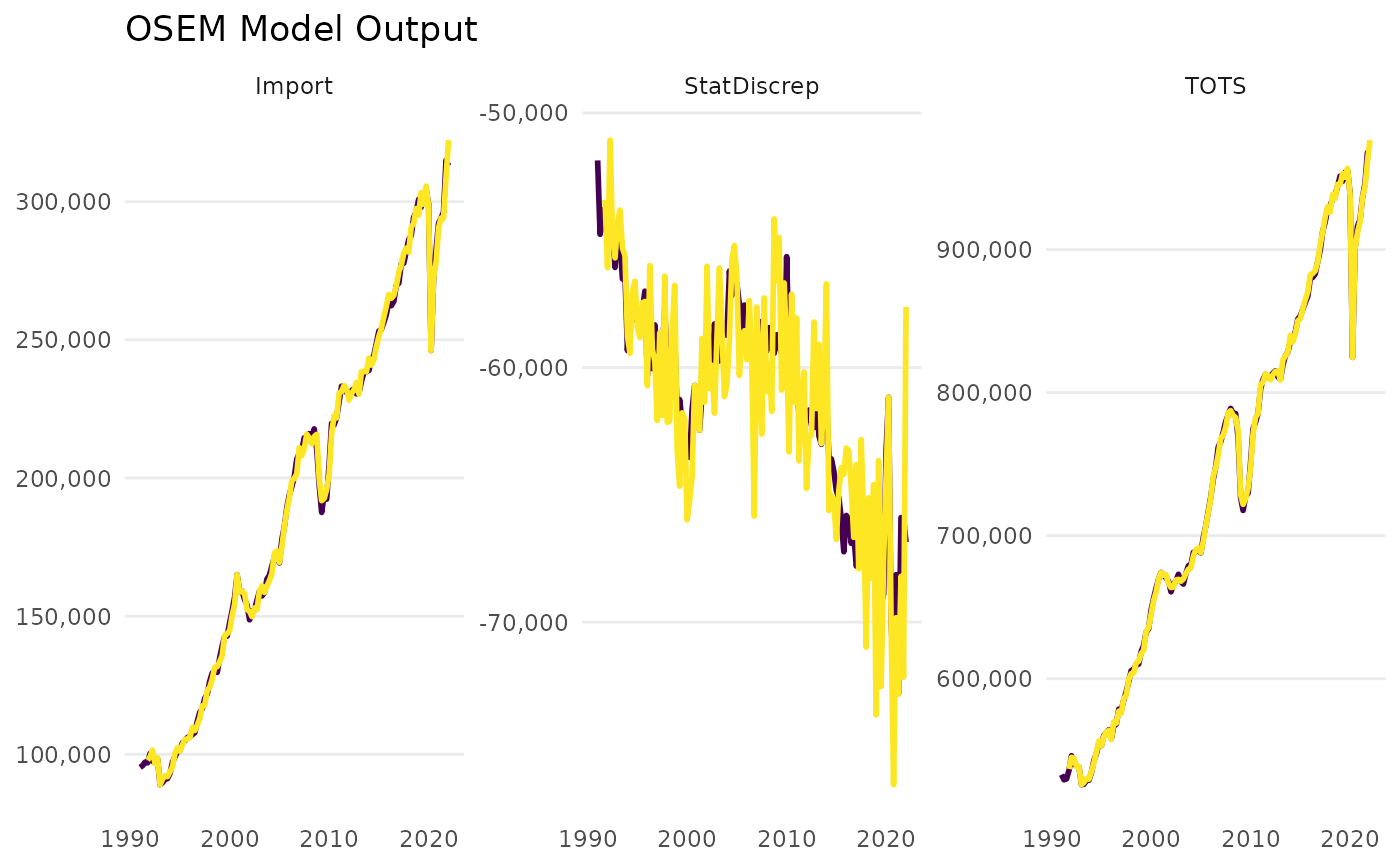

run_model(specification = spec,

primary_source = "local",

input = sample_input)

#>

#> --- Estimation begins ---

#> Estimating Import = FinConsExpHH + GCapitalForm

#> Constructing TOTS = GValueAdd + Import

#> Constructing StatDiscrep = TOTS - FinConsExpHH - FinConsExpGov - GCapitalForm - Export

#> OSEM Model Output

#> -----------------------

#>

#> Estimation Options:

#> Sample: 2010-01-01 to 2022-04-01

#> Max AR Considered: 4

#> Estimation Option: ardl

#>

#> Relationships considered:

#> # A tibble: 3 × 3

#> Model `Dep. Var.` `Ind. Var`

#> 1 1 Import FinConsExpHH + GCapitalForm

#> 2 2 TOTS GValueAdd + Import

#> 3 3 StatDiscrep TOTS - FinConsExpHH - FinConsExpGov - GCapitalForm -…

#>

#>

#> Relationships estimated in the order: 1,2,3

#>

#> Diagnostics:

#> # A tibble: 1 × 8

#> `Dependent Variable` AR ARCH `Super Exogeneity` IIS SIS n

#> <chr> <chr> <chr> <chr> <int> <int> <int>

#> 1 Import 0.308 0.790 0.016** 0 3 50

#> # ℹ 1 more variable: `Share of Indicators` <dbl>

#> OSEM Model Output

#> -----------------------

#>

#> Estimation Options:

#> Sample: 2010-01-01 to 2022-04-01

#> Max AR Considered: 4

#> Estimation Option: ardl

#>

#> Relationships considered:

#> # A tibble: 3 × 3

#> Model `Dep. Var.` `Ind. Var`

#> 1 1 Import FinConsExpHH + GCapitalForm

#> 2 2 TOTS GValueAdd + Import

#> 3 3 StatDiscrep TOTS - FinConsExpHH - FinConsExpGov - GCapitalForm -…

#>

#>

#> Relationships estimated in the order: 1,2,3

#>

#> Diagnostics:

#> # A tibble: 1 × 8

#> `Dependent Variable` AR ARCH `Super Exogeneity` IIS SIS n

#> <chr> <chr> <chr> <chr> <int> <int> <int>

#> 1 Import 0.308 0.790 0.016** 0 3 50

#> # ℹ 1 more variable: `Share of Indicators` <dbl>

# }

# }